How To Create a Realistic Budget and Define Intrinsic Ministry Values

Published in Insight - Spring 2015

By: Rebecca M. DaVee, CPA and Kari Eaton, Staff Accountant

In a world of finite resources, individuals and organizations tend to use an annual budget to ensure that resources are allocated appropriately and spent wisely. The annual budget is a helpful tool that allows a church or ministry to look strategically ahead at the upcoming year and plan, based on specific ministry “ROIs,” where it will invest its time and budget dollars to achieve projected outcomes. Because a church has finite resources, it is necessary to monitor and adhere to the operating budget closely. The typical budgeting goal of most churches is to “break even” or in difficult economic seasons, incur a nominal cash loss. Again, this process is especially important for churches because income tends to be more limited. An understanding of basic budgeting terms and budgeting approaches, can help you create a realistic budget so your church can steward resources and build reserves.

First, it is necessary to understand how churches spend their money in general. This information will be the foundation for how the budget is created.

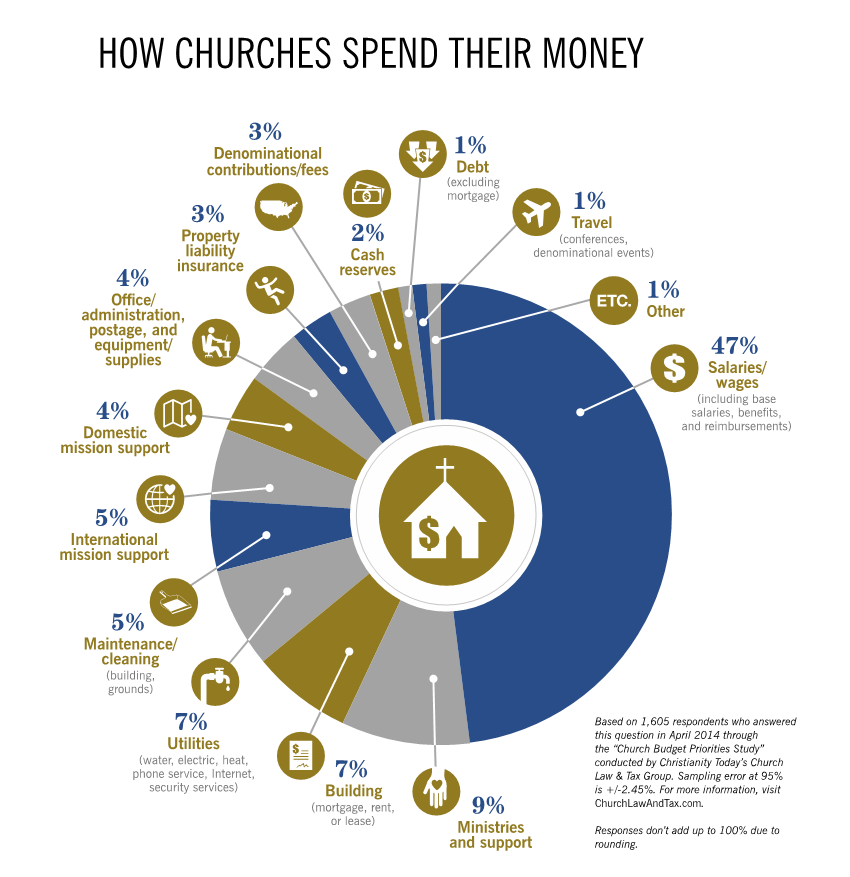

The pie chart shows a breakout of church expenses based on a national survey of churches (1,605 respondents in 2014 ). Based on the study, nearly half the church budget was allocated for salaries and wages for church staff. In general, the next largest portion (when combined) supports the church’s occupancy (facility) needs: building, utilities, rent, supplies, etc., which represent approximately 29% of the budget. Missions and outreach, internal and external, represent 18% of the budget.

Now that we understand how churches spend their money, let us look at budgeting basics. There are two key principles churches need to embrace when creating the annual budget: accountability and terminology. Many churches misinterpret accountability as simply accounting for where funds are spent. Accountability goes beyond just accounting by evaluating whether resources are spent wisely and are being used to meet measurable goals (ROIs) set by the ministry leaders. The difficulty that churches normally face is measuring outcomes (i.e., spending money wisely/strategically). It is easy to measure the amount of money being spent (when it is gone, it is gone). But truly evaluating the worth or “effectiveness” of the money spent becomes much harder.

One way to evaluate the worth of the resources being spent is to determine value received. I understand, that this is easier said than done. What did the church receive or what intrinsic value was increased by the exchange of cash and resources? I recommend creating a ministry leadership team (include 1 or 2 number crunchers) so that the church can critically evaluate the “use of ministry dollars” expended for designated projects, events, etc.

The second key principle is “terminology” and defining uses, roles and responsibilities. Many churches do not have a trained accountant or a CPA on staff to review financial transactions. Churches typically create a finance team with different roles to review and assess the church’s financial health. For most churches the finance team includes

•

a bookkeeper who is responsible for processing/recording the transaction,

•

a treasurer who oversees the bookkeeper and safeguards the church assets,

•

a church business administrator who oversees the church’s day-to-day operations,

•

a finance committee who focuses on specific financial decisions like the budget, and

•

an administrative board who approves the budget and monitors operating activities.

A number of churches require a congregational vote to approve the annual budget. True transparency is created when the church produces an annual report that includes financial reports and program accomplishments (outcomes). True accountability occurs when the financial statements are audited internally and externally and results of those audits are provided to the congregation (requested or not). Through the clear definition of roles, along with the clear goals of the church, the financial team is capable of reviewing transactions and church activity to ensure money is not just being spent, but strategically invested.

Let us consider the various approaches to the annual budgeting process. As we noted above, problems often arise because of poor planning and a lack of clearly stated goals. When starting the budgeting process, ministry leaders must critically define the strategic ministry goals/objectives of each department supporting the church overarching mission. In the perfect world it is ideal to plan ahead and have leadership formally agree on the mission directives of the church. Goals should not only be clearly defined, but must also measurable so that activities can been evaluated for effectiveness. While the goal “to assist those in need” is a valiant goal, how does the church measure effectiveness? Of course, this is not easily attained. Churches must create both long- and short-term strategic goals. Leadership must consider the ever-changing economy, geography, and demographics of the congregation. This is the start of the budgeting conversation.

The budgeting process is time-consuming, yet a necessary process. Among other things, budgeting:

•

Formulizes planning

•

Reduces emotional battles (agree on strategic goals first)

•

Becomes the basis for performance evaluation

•

Provides a source of control and authorization for the church to spend money

•

Assists in communication

•

Allows members to get involved

•

Increases the commitment to give

•

Serves as a source of confidence for church leaders

Budgeting is only a financial tool, a way to evaluate/manage effectiveness. Let us look at several common approaches to the annual budget:

•

Top-Down

•

Bottom-up

•

Incremental

•

Effective and strategic (programmatic)

Some churches adopt the

top-down approach. In this method, all budget development takes place at the highest levels of the church (i.e., administrative board, deacon board, board of directors/trustees, etc.) and the ministry leaders (including committed volunteers) and congregants are informed rather than included in the budget process. This approach typically takes less time and energy and mandates an outcome; however, it does often yield to discomfort among the committed church members who feel excluded from the budgeting process.

An alternative approach is

bottom-up budgeting. This allows for as many people as possible to be included in the budgeting process. Typically, the church’s financial team develops revenue assumptions and

guideline then asks teachers, deacons, members, etc., for input in creating the final product. The advantage to this approach is that the people who invest their time and energy are also using the funds daily and are directly involved in the budgeting process; they are more in touch with the actual cost of church activities, however, this approach may take longer and lead to quarrels among members/departments with opposing views and agendas.

Top-down and bottom-up approaches are ways to communicate financial information – not a method of evaluating effectiveness. The

incremental approach utilizes historical data, estimates a current year cost and voila - the budget is actually formed. Incremental budgeting is simple to use, easy to understand and the fastest to create. If you need fast and easy – this method is for you. This approach focuses solely on cost, not accomplishments, and does not allow room for a changing future.

As I emphasized earlier, I recommend the

effective/strategic (programmatic) method. It includes all three methods and realigns the purpose of the budget with the strategic goals for the upcoming year. Evaluate prior year activities/costs, determine the intrinsic value received/created, develop upcoming goals/objectives and estimate the cost. This budget method requires a significant amount of time and communication.

While there is not one certain right or wrong way to budget, it is abundantly clear that this process is always necessary. Without budgeting, monies are more easily spent without a just cause, and programs will go on without being measured for their intrinsic exempt value. The finite resources churches receive must be accurately accounted for and allocated properly to maintain a successful ministry. Budgeting is a tool and roadmap to keep the church on track. Through thorough planning and effective communication with ministry leaders, along with the information on budgeting approaches, the church can create a budget suited to meet their exact needs and to strategically plan not only for the upcoming year, but possibly the short-time cycle of 2-5 years.

Rebecca DaVee, CPA, can be reached at

bdavee@broadwaybc.org.